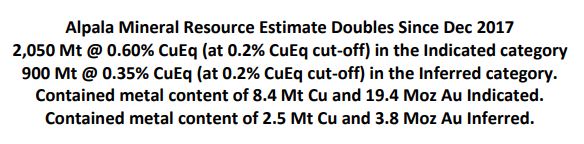

So, SolGold put out an updated resource statement for Alpala (link).

On the surface a massive jump on the previous numbers.

|

| The Contained Gold number should be Moz not Mt |

So what? They have nearly 3Bt of resources at overall grades that, even if it was at surface, would be regarded as being marginal.

|

- 2530Mt @ 0.28% Cu and 0.13 g/t Au or 0.37% CuEq

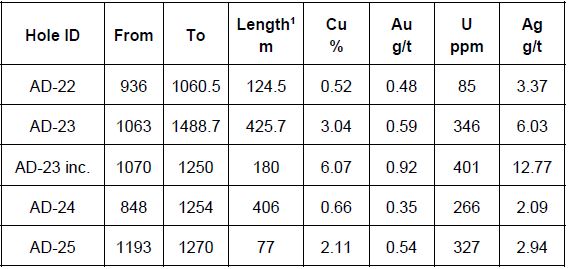

Let us look at the high-grade zone

I used the 0.9% CuEq values in the table, so they have:

- Indicated - 400Mt @ 0.9% Cu, 0.93 g/t Au or 1.49% CuEq

- Inferred - 20Mt @ 0.72% Cu, 0.52 g/t Au or 1.05% CuEq

Here it is

|

| best areas start at ~750m depths |

You can see that the bulk of the high-grade resources are in the central zone, which has been extensively drilled, and doesn't seem to have much expansion potential.

The Alpala Southeast zone appears to be defined by a couple of drill-holes, and is open in several directions, but it doesn't look to be very big.

We see the same with Alpala NW and Trivinio, but man is it deep.

The project that I was hoping to see some results from Aguinaga was a bust, and basically used the latest resource update as an opportunity to take my (small) profits and walk away, as for me, this is where the project doesn't quite make it. I've annotated a nice summary chart from Macquarie's nice summary on various block caving proposed projects (link), and we see:

I hope that Newcrest come in and take them out (link), but with the grumblings from Ecuador regarding their permitting issues (link), for me the story is over, especially as they'll need to raise more funds for their, in my opinion, extremely expensive exploration programs.