You have to give credit, Serengeti's team have been hard at pounding the the bald-headed moose, cranking the shank, and feeling their way around Kerwanka.

However, the problem with dancing with the one-eyed driller is that once in a while you have to consulting with your silent partner to see if the project is good enough for a one gun salute.

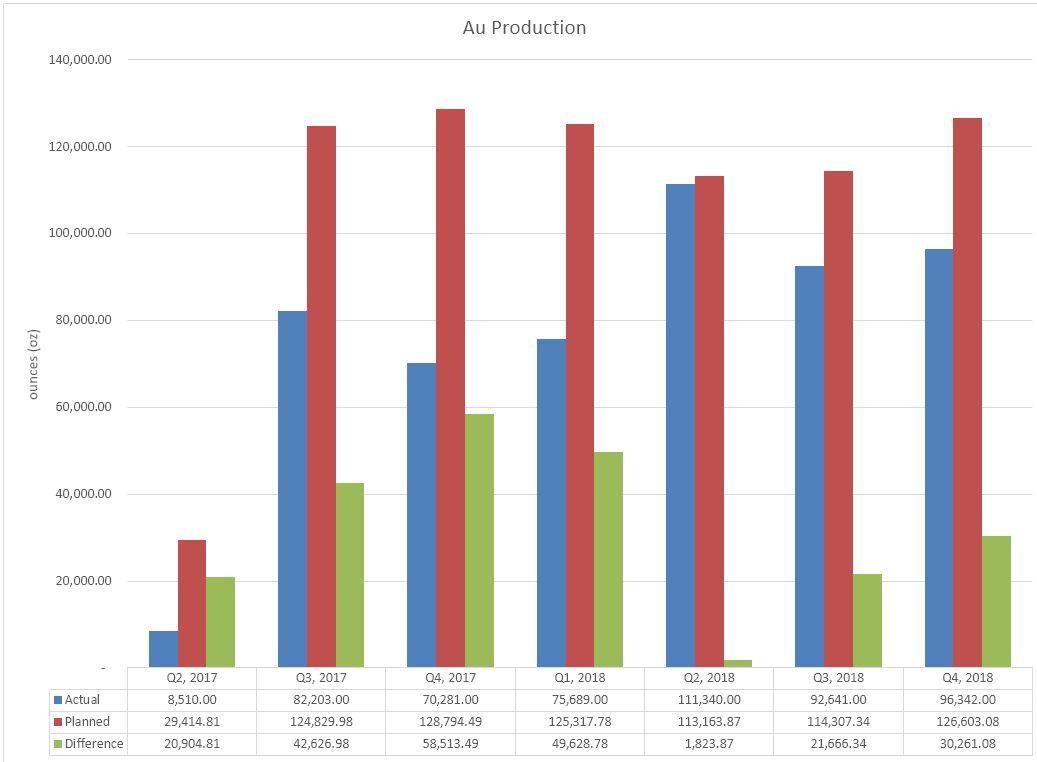

So why don't we stop serenading Mrs. Palmer and her five daughters by letting go of the one-stringed guitar and have a look:

|

| what a load of crap |

So basically, they could define >10 billion tonnes at a similar grade and it would still be too shit to put into production.

For amusement, here is the Kerwanka underground resource plotted against the mighty proposed block cave operations

|

| Well, someone has to come last... |

So basically, all that hard work milking the moose, fly fishing and hoisting the petard still means that the project is crap. That's enough to make the the bald man cry