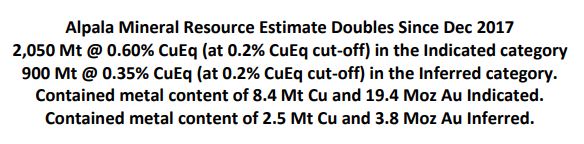

So, SolGold put out an updated resource statement for Alpala (link).

On the surface a massive jump on the previous numbers.

|

| The Contained Gold number should be Moz not Mt |

So what? They have nearly 3Bt of resources at overall grades that, even if it was at surface, would be regarded as being marginal.

|

- 2530Mt @ 0.28% Cu and 0.13 g/t Au or 0.37% CuEq

Let us look at the high-grade zone

I used the 0.9% CuEq values in the table, so they have:

- Indicated - 400Mt @ 0.9% Cu, 0.93 g/t Au or 1.49% CuEq

- Inferred - 20Mt @ 0.72% Cu, 0.52 g/t Au or 1.05% CuEq

Here it is

|

| best areas start at ~750m depths |

You can see that the bulk of the high-grade resources are in the central zone, which has been extensively drilled, and doesn't seem to have much expansion potential.

The Alpala Southeast zone appears to be defined by a couple of drill-holes, and is open in several directions, but it doesn't look to be very big.

We see the same with Alpala NW and Trivinio, but man is it deep.

The project that I was hoping to see some results from Aguinaga was a bust, and basically used the latest resource update as an opportunity to take my (small) profits and walk away, as for me, this is where the project doesn't quite make it. I've annotated a nice summary chart from Macquarie's nice summary on various block caving proposed projects (link), and we see:

I hope that Newcrest come in and take them out (link), but with the grumblings from Ecuador regarding their permitting issues (link), for me the story is over, especially as they'll need to raise more funds for their, in my opinion, extremely expensive exploration programs.

What a load of tosh. The biggest recent discovery. A tier 1 asset. Big mining companies buying in.

ReplyDeleteMust be an ulterior motive in play here.

Which would be? I just think that it isn't quite big enough to make it. If or when BHP or Newcrest fight over it and you all become millionaires, you can laugh at me.

DeleteIt's no tier 1 resource in my view, nowhere near big enough nor rich enough to be tier 1. Keep in mind that reserve grade (and tonnes) will drop (from resource grade & tonnes) when reserves are estimated. When mining shapes are defined maybe you get 300 million of the 400 million > 0.9% CuEq, and maybe you have to take another 100 million of lower grade surrounding material inside the cave boundary.

DeleteThe McQuarrie chart mixes reserves (El Teniente) with resources so the lines for green and brownfield are likely higher than shown. Despite that they clearly show that this deposit needs a lot of work on both grade and tonnes to become a tier 1 project.

I read the McQuarrie block cave report. It describes block cave mining very well. One point in their open pit comparison....they assume a mining cost of $5,00/t, which implies a strip ratio of roughly 1.5 at a $2.00/t cost/t mined. If the strip ratio is higher than 1.5 then the cost parameter begins to favour block cave.

DeleteUpcoming copper deficit replete with a dearth of good new copper projects. Untested targets on the property and good existing infrastructure. Newcrest and BHP are chomping at the bit. They are obviously aware of something AG has missed.

ReplyDeleteThere are massive amounts of lower grade surface deposits if the price jumps up. One concern is that there aren't many greenfield block cave projects coming into production. Projects like Resolution and Golpu (which have better overall resource grades) are still at the feasibility stage (the last technical report published on Wafi-Golpu is from 2012).

DeleteI have no problems that the deposit is good, I just don't think it is big enough, and decided to take my (small) profits now.

It's always good when a major is on your side but it's no guarantee that the project will proceed to production. Pebble comes to mind. Three majors have gotten involved. One spent $500 million before walking away.

DeleteNobody ever went broke taking a profit,the sidelines just might be a good place to be while copper prices and more drilling tell the future.

ReplyDeleteThanks, the other concern I have (which has been reduced by the Newcrest purchase) is SolGold's burn rate and the fact that they would need to raise a lot of money in 2019 to keep exploring.

DeleteWhat could be nice is for Solgold to spin out their non-Alpala assets into s new company because at the moment they aren't getting value from them.

exactly, and I don't think it is a good enough project for a company to pay ~$1B for it.

ReplyDeleteI agree, I just see (unless BHP and Newcrest go crazy), that this project will sit there and SolGol will keep diluting to raise the funds to advance it.

ReplyDeleteHe's making a list and checking it twice....going to find out who's naughty or nice...

ReplyDelete"Change of control" means severance for the key executives of one or both of the precursor companies.

ReplyDeleteThree Atacama executives (Albrecht Schneider, Carl Hansen and Thomas Pladsen) were eligible for change of control severance of 3/4 of a mil each. (Not a bad gig if you can get it.) The information was publicly available in the Management Information Circular, published in advance of their 2017 annual general meeting. Also of interest in that report...none of the executives had been paid for 2016, so their salaries plus accrued vacation time for 2016 were also part of their severance unless paid prior to the corporate amalgamation. Essentially the company was broke.

ReplyDeleteSee note 13 (Exploration Expenses) of their Sept 30 financial report. Total spent for 3 months was $99,875 and for 9 months (2018) was $388,475. Of this amount $264k was spent on technical consultants, $71k on geology, $54k on community relations. Looks like nothing was spent on drilling, although they had a drill program going at Fenix in the 4th qtr.

ReplyDeleteI'm no accountant but I think I know my way around financial statements. Theirs should be pretty simple one would think but....no. I looked at their cash flow statement to see what they did with the $10m. The only changes were their costs for the quarter and their financing. The costs are there. The financing shows up. But their cash balance seems to be on the low side for some reason.

ReplyDeleteI see what they did. In their Sept cash flow they show costs to acquire Atacama, the Atacama options and the Atacama warrants. Against this they credit the asset, but at $3.25 million less than the above three costs. All of these are non cash, so it's strange that they would be on the cash flow sheet as they aren't on the income sheet. There is no explanation of where they came up with the value for Fenix.

ReplyDeleteThe project they bought is a low grade gold leach...iffy at current prices

ReplyDeleteIf you want earn money or increase your revenue contact us now

ReplyDeletewww.toprankingseo.net search engine marketing

"I enjoy reading your post guys,,, just keep posting. Anger Quotes

ReplyDelete"