I've been casually following them and Soledad and I've always though that the breccia pipes are very small, and if there is a porphyry on the project, it would be too deep to do anything with.

So, I've finally managed to compiling the data into leapfrog (link).

We can see that Chakana have drilled 25Km of drilling but appear to have 4 of the ~27 breccias identified so far on the project.

|

| Breccias everywhere |

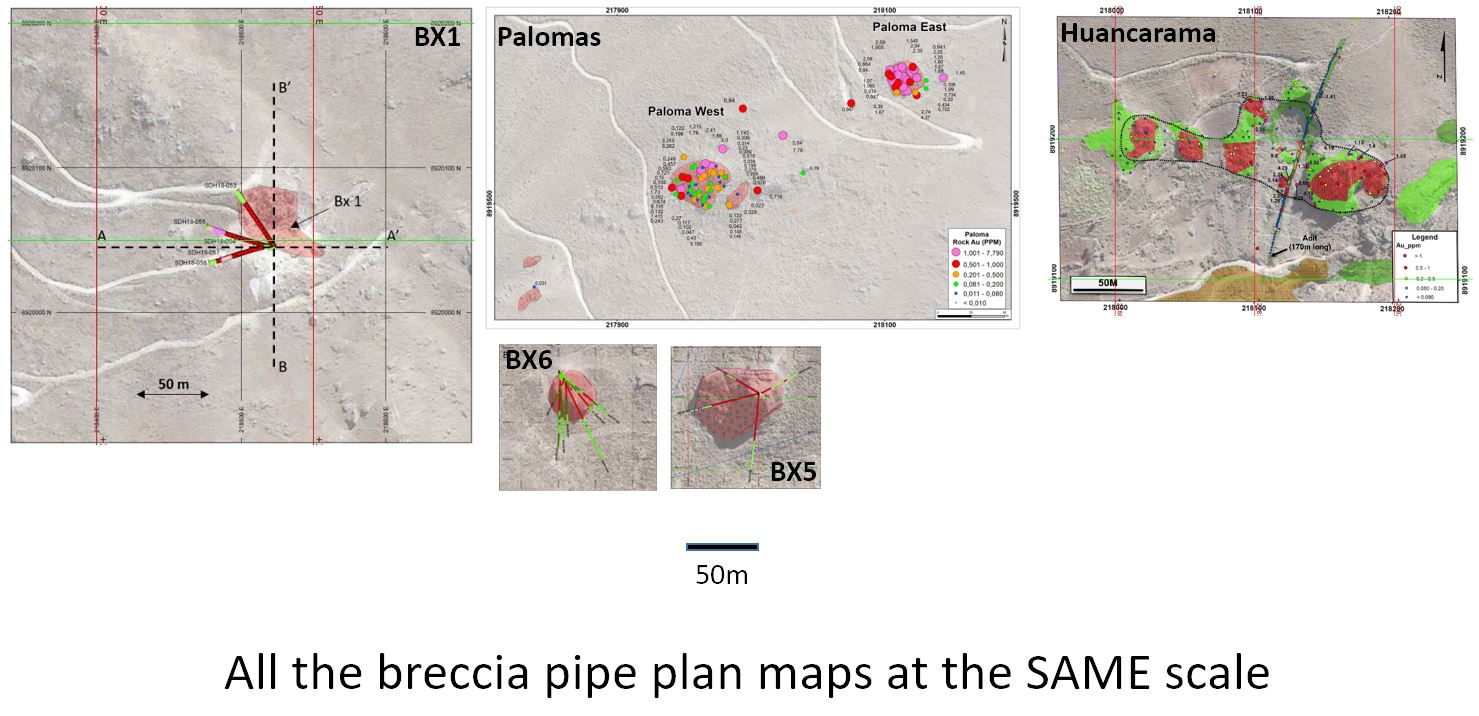

Essentially the breccia pipes are very, very small, typically with a 50m x 50m surface expression, based on the 5 breccias that we have maps for.

BX1

This has received the most drilling and has produced the best results.

We can see that lots and lots of holes have been drilled down the guts of the BX1. However, unlike BX5 and 6 below, a few of the holes intersected a blind breccia body to the SW.

It also appears the the grades are decreasing with depth, but this may be a result of the holes leaving the breccias and drilling country rocks, but we can clearly see, the breccia body is small (75m x 25m with 300m vertical extent - of the >2% CuEq mineralization), but high-grade.

BX5

More drilling down the guts of the system, it is 50m x 50m, and has been drilled to 200m depth. It is lower grade than BX1, but consistently over 1% Cu. However, I'm not sure that this is good enough for a body that will be mined from underground, it may need to be >2% to be viable.

BX6

BX6 is another small breccia body, with more drilling down the middle. We have a high-grade (>3% CuEq) close to surface (supergene enrichment), before the hole pass into moderate grade breccias below. Nothing special here

I'm going to stick with my original opinions, even though BX1 shows that there are additional breccias that don't reach surface, I'm not convinced that Chakana will be able to define a significant resource at the project. They have enough drilling into the BX1, BX5 and BX6 breccias to give the market something, but my back of the envelope notes come up with ~2Mt, which isn't very much.

I can understand them flogging the porphyry potential. This is a valid model, but on their own sections they suggest that any porphyry body will be very deep and essentially unexplorable.

However, they have money from Goldfields, and would like them to move away from BX1 and drill a few holes into 5-10 different breccias to see they have other high-grade breccias similar to BX1 (e.g. Faro and Corral in the Western Breccia zone).

Unless they find something amazing, and demonstrate that they can find enough breccias to define ~5Mt of material grading >2% CuEq, I don't see much value in the project on its own. However, with Hercules next door, could there be potential synergies with Lincuna? If the breccia bodies could be mined profitably from underground, maybe Lincuna would like some highly profitable ore to process (as long as it isn't too expensive to add a copper circuit to their mill)?

So Goldfields missed that? They bought in at that kind of premium for teensy little pipes and non economic porphyry potential at depth? I find it hard to believe that you can demonstrate with simple leap frog models that there is no value here and the team from one of the world's largest gold producers got suckered. Wouldn't they have taken the same two seconds to run the intercepts through geo software? Occam's razor would kind of hint at there being information in the Chakana data room that assuages concerns about size/scale etc and my suspicion is that, as you mention, they are eyeing the potential of all the pipes yet to be drilled and all the drilling on the pipes yet to come.

ReplyDeleteReaders of this blog, which I do enjoy immensely, could be forgiven for responding to your statement, "I'm not convinced that Chakana will be able to define a significant resource at the project." with a chuckle and "Goldfields is, to the tune of $8 million".

Fair?

$8 million is nothing to Goldfields. They know the same as everybody else, and they are speculating just like everybody else as well. You go to the poor house pretty quick thinking that the majors are somehow aware of stuff that the market is not able to discern ... that theory is right about 5% of the time.

DeleteHello Anon,

DeleteFair comment. For me, the key event in 2019 is if Chakana will publish a resource calculation for the BX1, BX5 and BX6 breccias.

If they don't, which wouldn't be due to lack of drilling, it would demonstrate to me that the bodies are too small and won't add up to a significant resource.

The porphyry - slight clarifying statement, I mean it as uneconomic to explore as it would be very deep (potentially 1000m+)and simply too expensive to drill.

This comment has been removed by the author.

DeleteAG is calling it like it's seen given the publicly available information.

DeleteI looked and felt the same (minus the in depth technical DD) as I've seen a bunch of Breccia pipe plays - very hard to build tonnes. Sure they are looking for the source - but aren't we all. Find it, then I'll pay a premium.

And I give zero poops about Goldfields. Biggies make mistakes on the regular and for a multitude of reasons. That said, i hope they find the motherlode.

"AG is calling it like it's seen given the publicly available information." - exactly my point. Publicly available information plugged into Leap Frog. Just intercepts. If you're drawing conclusions from that and considering this blog post to supersede everything else...well, then I suspect you miss a lot of opportunities or do, in fact, pay a lot of premiums.

DeleteI wouldn't go so far as to say "Biggies make mistakes on the regular" as I don't really think that's fair. Hindsight is always 20/20 and DD isn't infallible. Was never my point to suggest otherwise. One goes with the evidence one has. And they have more than us and based on what might be at Soledad it will take more than an elementary leap frog work up to dismiss the project. OBVIOUSLY, the team at GF would have done at least that, and more. Plus a site tour (or several) plus a data room plus numerous conversations with the company and it's people and so forth. I'm not saying this is a sure thing or even a great bet...I'm just saying this is "report" should be taken in context and for what it is.

Goldfields.... Let me think...Woodjam? Yes Woodjam anyone? $14 million for 227 MT of... wait for it.....0.31% Cu. No appreciable gold. Under 40m of till. And for there efforts they have an NSR and about $750,000 in shares of WCC. Makes sense why they drove Chakana to the ground, after getting their fingers burned.

DeleteTo Anonymous....many majos invest in juniors and lose their money. Look at Pebble where over $500 million was spent by at least 3 majors on a world class deposit. But you are correct to point out that Goldfields has access to information not available to the public.

DeleteI think the questions is, what are Goldfields looking for? You would expect them to invest in projects with the potential to host >2Moz Au at a decent grade (say >1 g/t Au for open pit and 3g/t Au for underground).

DeleteDoes Soledad fit in with that? To me no. Is this good news for Chakana, having a partner/shareholder that has given you a lot of money, but will not really be interested in the final outcome as to me the project will always be too small and not contain enough gold to interest them.

From the NR: “Gold Fields was exceptionally thorough in their due diligence, bringing a large multi-disciplinary team to site and reviewing all major aspects of the project from a mining, environment, and social perspective, ” Chakana’s president and CEO, David Kelley, told The Northern Miner. “Gold Fields was impressed with the upside potential of Soledad, not just the large number of tourmaline breccia pipes we have yet to drill, but also the potential of a much larger deposit driving the breccia pipes.”

ReplyDeleteNo-one is going to say that they didn't do a thorough due diligence!

DeleteThere will be a larger body driving the breccias, but I feel that it will be simply too deep to drill.

Major mining companies have no issues throwing around small amounts of money (look at Newcrest and their ~$20M invested in Azucar) at interesting projects. They play the long game and spread out their investments and hope that 1 out of 10 or 20 or 50 work.

Well that is the plan . . .to "drill a few holes into 5-10 different breccias" this year. Management understands they need multiple high grade pipes to create a viable project and the best targets are lined up and ready to go once the permit arrives. A few more Bx1s and the company will be in business (assuming pipe spacing is workable).

ReplyDeleteNot a threat to Kamoa/Kakula then???

ReplyDeleteOnly if Bob Friedland decides to visit, slips, trips and falls off a cliff...

Delete