Summary

- Good

- Great result from hole CHR-002

- but, we have grade smearing, outside the >2% zone, it drops off to 0.84% Cu, still good, but could be marginal for an open pit operation

- Small, near surface oxide zone

- Some other interesting targets to be tested around the property

- Bad

- It was a shame that they went with cheapo RC drilling option as it meant:

- Hole 002 terminated in good copper mineralization

- Holes 004 and 005 couldn't reach the extension of this zone.

- Typical grade 'expansion' - the high grade (>1% Cu) is found in narrow zones surrounded by low grade (0.2-0.3% Cu).

- Trench samples look good, but I'm skeptical of trench sampling as:

- remember - you can bias them by sampling along a mineralized structure rather than sampling across it - the FAG will explain how you can 'improve' your trench results

Is water, or the lack of, going to be an issue?

There are advantages and disadvantages with using an RC rig:

- Advantages

- Quicker - drill 200-300m per day compared to 50-100m for a diamond drill

- A lot cheaper - ~50% of the cost (or even cheaper) of a diamond rig.

- Doesn't need water - very useful in the Atacama desert

- Disadvantages

- Lower quality geological information

- greater deviation - the holes drilled by Camino started at 45 or 50 degress, but steepened to almost 80 degrees at the end of the hole.

- if you see any company not-surveying RC holes, that is a good sign that they don't know what they are doing and that the data from these holes are suspect as they can't accurately tell you where the mineralization is located.

- bigger visual impact

- require more site preparation - wider roads, larger pads

- generally limited depth - ~300m depth is generally the deepest you can drill with RC

- can have grade issues - smearing of grade, especially at the water table

TL:DR: They started off good, but by using the wrong equipment, they have are not maximising the value they are getting from teh drilling (unless drilling magnetite-rich zones is the objective).

Geology Wank

Hole CHR-002, very good zone, but as the hole stoped in mineralization we don't know how wide it will be.Follow-up holes 003, 004 and 005 intersected the upper copper oxide zone, but due to hole deviation, which is common in RC drilling, they all steepened and didn't reach the target. The irony is, this deviation was seen in holes 001 and 002 and I would have expected Camino to have modified the program accordingly, as they showed us that there was a very high probability that holes 004 and 005 would have steepened (go more vertical) and not hit the copper zone.

I'll explain it visually, I prepared this image form the original press release

- Red line = planned hole trace (i.e. where they wanted the hole to go)

- Colored line = actual trace of the drill-holes

- Difference between these lines = the deviation

- we can see that as the hole gets deeper, the hole steepens (becomes more vertical)

- We can also see that the holes can only be drilled to around 300m - this is as far as this RC rig is able to drill at this project.

- Magenta line = what I think hole CMR-005 will do - it will hit the upper zone (my guess ~20m @ 0.6% Cu) and not reach the copper zone.

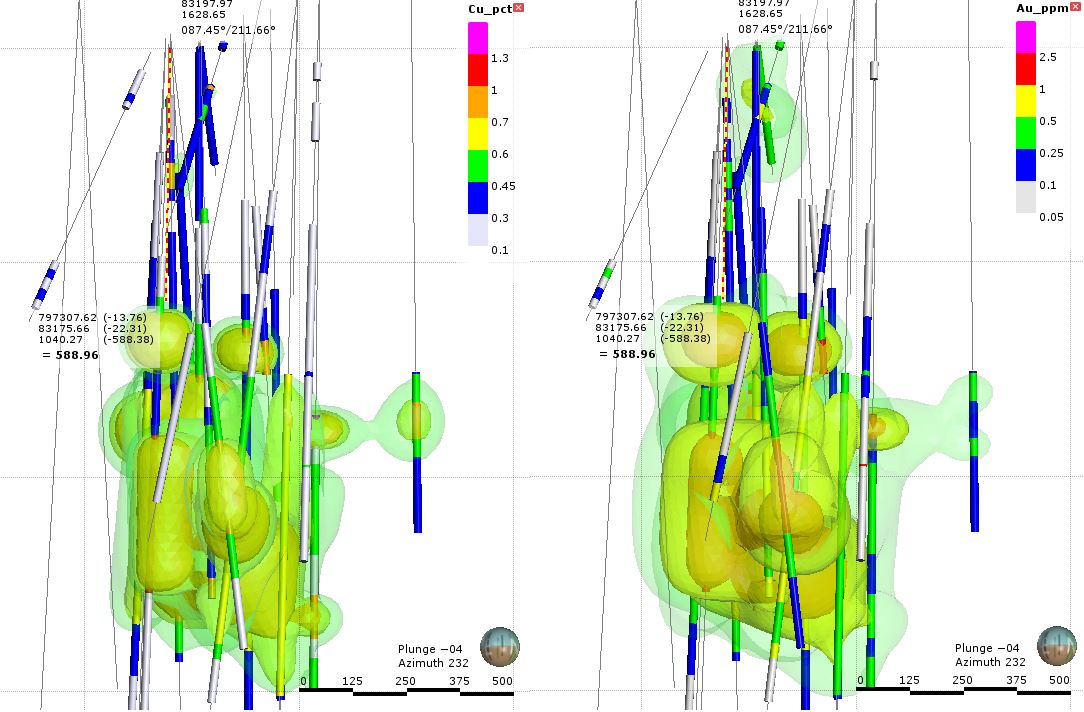

This is from the latest presentation

Look how much blue (0.1-0.3% Cu) is included in that 44m zone grading 0.86% Cu!

So you can see how much the holes are bending by (up to 20 degrees), and that makes it hard for the company to hit the planned targets, which is the reason why holes 004 and 005 missed.

You also need to think about the how the mineralization occurs, is it:

They look to be nearly vertical, indicating that this how the mineralization occurs at Adriana.If the deep mineralization hit in hole 002 is vertical, then that zone may only by ~ 40m thick.

I think That Camino need to rethink their drilling strategy! They need to get some diamond rigs up there to answer questions on controls and size of mineralization. Continuing to drill RC-holes will start to reduce the value the company obtained from hole 002.

I've created a quick model of the drill-holes with their sections, so you can see how all the holes relate (link).

Look at how the Magnetite rich zone changes between sections...

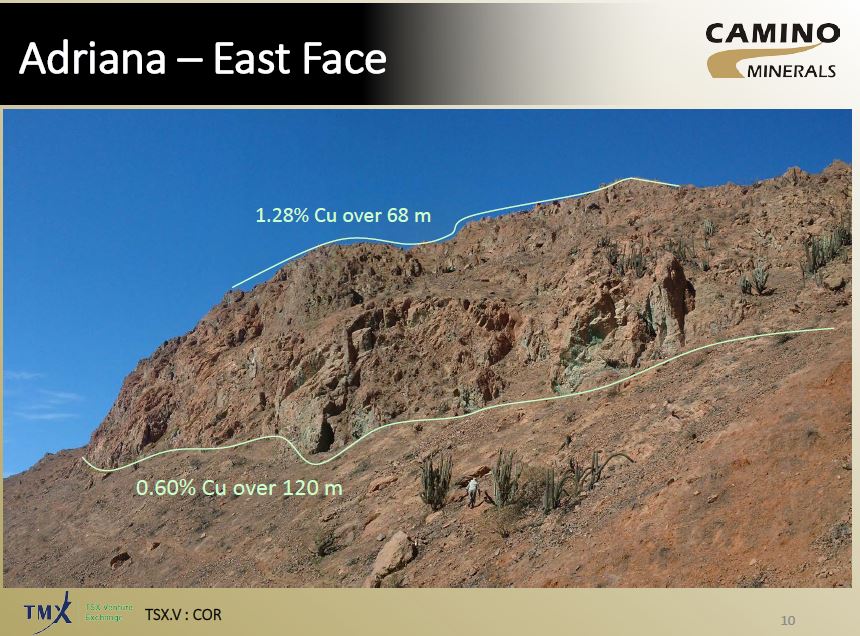

and some photos of some old workings

I've annotated the mine photo to show how you can get Maximum Impact (tm) results from trenches.

We have 2 trenches

|

| bendy drillholes |

|

| so that makes them 0 from 3 |

So you can see how much the holes are bending by (up to 20 degrees), and that makes it hard for the company to hit the planned targets, which is the reason why holes 004 and 005 missed.

You also need to think about the how the mineralization occurs, is it:

- flat lying bodies

- Steeply dipping narrow zones

- large stocks

They look to be nearly vertical, indicating that this how the mineralization occurs at Adriana.If the deep mineralization hit in hole 002 is vertical, then that zone may only by ~ 40m thick.

I think That Camino need to rethink their drilling strategy! They need to get some diamond rigs up there to answer questions on controls and size of mineralization. Continuing to drill RC-holes will start to reduce the value the company obtained from hole 002.

I've created a quick model of the drill-holes with their sections, so you can see how all the holes relate (link).

Look at how the Magnetite rich zone changes between sections...

Trenching results

Hello, FAG here. Camino have given us some nice photos of some green-stained rocks in the Atacama. |

| Clouds!!! |

|

| Azurite skies... |

|

| Mein Mine |

I've annotated the mine photo to show how you can get Maximum Impact (tm) results from trenches.

|

- Trench 1 - running parallel/along with the copper zone

- Trench 2 - running perpendicular to the copper zone

Which will give the 'best result' for your press release?

- Trench 1 = 30m @ ~1% Cu

- Trench 2 = 3-5m @ 0.6-1% Cu

The question you need to ask is:

Mineralization

This was covered in the IKN post, so I've just included a image of a simplified mineralization zoning in a copper deposit

So, the upper zone is primarily oxide material, it may have some native copper and copper wad that is insoluble accounting for the 25% of the material that isn't acid soluble.

However, the lower zone is high-grade, contains only 25% soluble material, I wonder if this hole hit the enriched zone and we have a lot of Chalcocite.