[Pretium quote]

They failed to do this (link) by falling 5% short of their lower guidance expectations, and just to top off the good news, we get a nice PR investigating the trading it is shares (link).

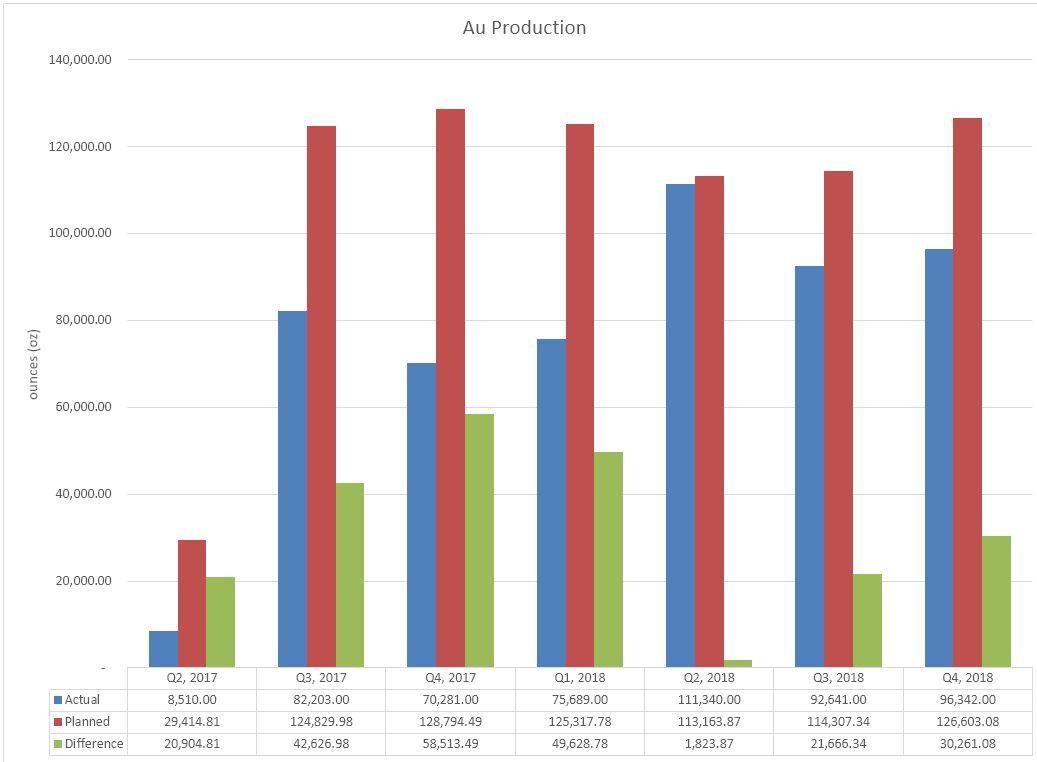

So how bad were the Q4 numbers?

Pretty shitty, there has been a consistent decline (but like my school grades) since the mine reached steady state production and the new grade control system came into place.

It is almost as if Pretium, by some coincidence managed to be mining some high-grade zones the same time. How fortunate.....

We can clearly see that only once (Q2), did production come close to the Feasibility Study number, and Q4 was a huge miss.

My bug concern, and I've mentioned this a few times, is what will happen to the grade once they ramp up to 3,800 tonnes per day?

If they manage to maintain the same average head grades (11.98 g/t Au) and recoveries (97%) that they achieved in 2018 (around 11.98 g/t Au) after the expansion we should expect quarterly production to be around:

- (90 x 3800 x 11.98 x 97%) /31.1 = ~128,000 oz per quarter

However, the common thing that happens when a mind finds itself with a hungry hungry mill, it that they chuck any old crap into it and the grade plummets.

I wonder what will happen here?

Mills do tend to be hungry beasts and have no consideration for mining personnel!!!

ReplyDeletePVG will probably be OK at 10 grams per ton/3800 tons per day if they keep finding gold to add to reserves and gold stays over $1250. My money is on KL, I love how they run their mines. Looking forward to KL reserve update in late February.

ReplyDeleteOk but the stopes are 15m by 30m, so any high grade zones have to be taken in those blocks, no selectivity finer than that, except for within grade control adjustments. They also have a sequence pattern to at least roughly comply with.

ReplyDeleteA full year averaging 11.98, The mineral reserve estimated region of close spaced drilling, slide 8, November, has a grade of only 14.5 and that is before dilution of say 12%, so it leads to a mill head grade of about 12.8, where the mined grade actually is not far off. The parameters for the model were a little high, but not by a huge amount. The higher grades to 16.5 are outside of the main VOK mining zone, to be mined in later years. Also it would not be good optics to exaggerate the aiming for best grades while production increase application was being considered. Regulators could expect numbers from mine to back up the reasons given for production rate increase. 128,000 ounces per quarter is not a negative. The tetra tech report page 16-17 explained the unrestrained production rate for the design was about 3500 tpd, so 3800 cannot be called pushing too hard.

The deposit has it's difficulties, but it had a strong mineralizing system, and it's large with lots of potential to increase an already large size.

18 months into production and all of the harsh outspoken critics have been wrong, every one of them (easily predicted). The over optimists were also expecting too much. Those with balanced moderate views were correct on this (easily predicted). Presumably they may not have many Cleo containing blocks to fall back on, but the rate increase will way more than compensate. The middle path was and remains correct, I think...

Regards, Paths from stockhouse

midpath@resourcepathway twitter

The mineral reserve estimate on Slide 8 includes dilution as mentioned in the FS of 12%, with recovery of 94%. We can't say if these are reasonable numbers because we don't have enough information. The question then becomes...is the amount of dilution more than the FS estimated? Alternatively, is the mineral resource estimate higher than actual results? Or perhaps both?

DeleteI agree with your comment on the higher grade expected later in the mine life. This can be clearly seen on P 128 of the 2014 resource report. However I would also point out that the estimation method used MIK. Every deposit I've seen that used MIK has been over estimated on grade.

The statistics on P 102 of that report show a mean grade of 2.57 g/t and a CV of 27. This suggests there is a heck of a lot of 2 gram material and a small amount of very high grade material. The West zone CV is better, with a CV of 11 but the average grade is also lower at 1.66 g/t. This zone may not be economic in the upcoming re-estimates.

It will be interesting to see their resource and reserve updates expected this half....what parameters they changed and why.

Anybody who has been unfortunate enough to follow your "middle path" so far has at best broken even (more likely lost money) on PVG, and never mind the opportunity cost. You gradually climbing off your high horse is not fooling anybody and there are still several rungs to go before you're grounded (in reality).

DeleteMarket price of shares has volatility reflecting the deposit variance, that does not mean the true value of the shares has dropped. My expectations have been in 12 to 12.5 gram range for over a year, no climbing down for me. That can still lead to 500,000+ oz. per year towards 3800 tpd. So many have been so critical, all the while as the company calmly produced 528,496 oz.'s so far. No problem.

DeletePaths, stockhouse id

They're mining the central and best-understood portion of this deposit (for a reason). Look at the block model. It shows outlying areas with (supposedly) much jucier grades. You being right very much depends on those areas with low density drilling actually turning out to have bulk grades ~10 g/t. Not saying it can't happen, just that it is super risky. Good luck sir.

DeleteThe grades on slide 8 are from the Dec. 15/16 news. Does not include dilution, as I read it. The main zone VOK grades are lower than surrounding grades which still have to have drill density increased. Paths,

DeleteThe title for the table (with the arrow) is "Valley of the Kings Mineral Reserve Estimate". Using the term "Mineral Reserve Estimate" means dilution has been considered.

DeleteBill of course is correct. Not only that, he made a point earlier about secondary stopes. They are going to generate lower grades for sure, so in effect we are already looking at the BEST grades these areas are going to generate. From the feasibility study:

Delete"The largest component of dilution at Brucejack will be paste backfill due to its inherently weaker strength compared to the hanging wall and footwall rock masses for any given dimensions of exposure."

It may be the dilution forecast in the feasibility was on the low side. A survey of longhole mining in Canada showed that 47% of mines had dilution over 20%. I was not concerned here, because the deposit does not have much in the way of hard boundaries. Most of the over break would still carry reasonable grades. The paste fill need not be a problem. When they know they will be mining against fill they will have used extra cementing agents. Anyways, it's clear things will still be reasonably good, the numbers are more than ok. Paths,

DeleteLack of hard boundaries on mining shapes is a problem not a feature. Yes you are right that if the diluted grade at blast shape boundaries after grade control are already low (as suggested by results) then the incremental zero grade from backfill caving in secondary stopes is minor. On the other hand, let's consider the primary/secondary stope boundary condition itself insofar as geology never conforms to statistics so therefore on average we should get the average mine grade at boundary not cutoff conditions. In which case dilution matters very much.

DeleteSome notes on the practical aspects of mining....

DeleteThe benefit of paste fill is not in additional fill strength, although it may have marginally higher compressive strength. The main benefit is a much faster fill cycle, which allows nearby stopes in the sequence to be mined more quickly. In highly stressed mines (This is not one of them to my knowledge) paste fill is essential to maintaining ground stability. I have had stopes literally begin caving because they were left open too long. This is fine initially, but quickly becomes a problem as the cave gets larger and enters adjacent stopes or even the hanging wall.

It's quite common in gold mines to put down a sill mat to recover gold fines that filter down to the stope floor. (We actually did this in nickel mines in Thompson Manitoba back in the '60's when I worked there.) In Pretium's case the stope floor is backfill. Mining will probably intentionally include a meter or two of the fill floor to ensure all of the filtered gold fines are recovered.

As I noted earlier, ring drilling, or actually the blasting has a significant effect on dilution. Secondary stopes cannot be fully silled out due to lack of ground support, so rings are a necessary evil. Ring holes drilled to the extent of the ore will damage fill in adjacent stopes, causing dilution. A mine can hold the holes short, but risks not recovering all of the stope as designed.

In sub-vertical ore zones dilution from the hanging wall can be a problem. Mines attempt to control this source through cables and straps on the hanging wall but this can only be done at the sub level interval (every 20 to 30 meters vertically) and only when the stope is fully silled out to enable access to the hanging wall. It is analogous to sowing a tear in a cloth but using only every tenth stitch.

Great info Bill and much appreciated! The hangingwall is one problem ... what about irregularities in primary/secondary stope sidewalls across the mining panel? If we are to believe they are proceeding in accordance with page 22-23 from their November 2018 presentation it would seem they are potentially changing the blast ring geometry in each round.

DeleteI think everyone was able to foresee Pretium's guidance miss...at least I was. Let's face it...they've had a grade reconciliation problem since startup, amounting to about 75% of reserve grade over the first 18 months. I was supportive of most of their grade control program and would like to know how reconciliation changed over the quarters. I would hope they were able to close the gap somewhat, given all the time and effort spent on the new program.

ReplyDeleteSome people may look at the Pretium experience as a failure. I believe that would be wrong. Few mines go through startup without issues. Look at the Copper Mountain experience and keep in mind that this was a brownfield start-up,not a greenfield like Brucejack. There are lots of positives at Brucejack, not the least of which is almost 400k ounces in 2018. What mine(s) in Canada out produced Brucejack? Throughput and recovery were excellent...kudos to the processing team. The mine is generating a lot of surplus cash, which means it is a worthwhile investment at some price. The only financial question I would have is whether they can manage the debt and still generate cash.

I think it's time to realize the mine will never achieve FS grades, which for whatever reason were overly optimistic. The reasons are not clear to me but model error appears to be the greatest issue and is one that cannot improve grade in the future. It would be useful to know if dilution missed the mark in the FS? I'm looking forward to the updated resource/reserve/reconciliation reports promised to be issued in the first half.

Using Taylor's rule (Hugh Taylor) one can estimate a reasonable mine output, and in this case it's 3,800 mtpd. So in theory the mine can bump up tonnage without affecting grade, as long as the infrastructure is in place..ventilation, stope development, dewatering, backfill system, mine equipment, etc. But in practice there are a lot of things that can go wrong and put pressure on the mine to fill that hungry mill. Have they mined any secondary stopes yet? If so, how were the ground conditions? The pressures of day to day operating issues will likely cause grade to drop. I hope they have a highly experienced mine supt.

I'm still bothered by the high coefficients of variation in the resource estimate and the very strange grade distribution where most of the tonnes are around 2 gram with a few tonnes at very high grades. Their reserve/resource updates should answer a lot of questions in that regard. They will have actual data for costs, productivities etc instead of guesstimates by engineers who have never actually mined.

Don't write this company off yet.

How is the grade distribution a mystery? They have two stages of gold with some remobilization. First you have the bulk stockworks at 1-2 g/t and then the VG with structural control (one of which is the Cleopatra vein, but not the main or only one). The VG form in a series of discontinuous sheets that meander along the stockworks and are preferentially developed near silicified hangingwall contacts that probably capped or controlled pressure changes in ore fluids. This is in contrast to the "raisins in a loaf of bread" model they want everybody to think as that better justifies their roughshod mining approach, which could potentially fail. The only way it does not is if outlying VG zones in the resource model turn out to be equal or better to those in the central zone they are currently mining. I don't think that warrants optimism.

DeleteThe ultimate goal is to mine it, which means you need know with confidence which parts of the mineralized zones are economic. Two gram material isn't ore. The CV is (to me) a measure of confidence in the estimated block grades. A high CV means a high probability that it's not there.

DeleteAs I have been saying for years now, there are solutions to the problem. I have often mentioned conditional simulation as a tool and I think it could be used here to good effect (not in terms of confirming the overall resource tonnage, but certainly in gaining higher confidence on mining shapes and grade). It seems I need to be more specific on this idea as nobody seems to get it. So I'll start providing concrete examples. I particularly like this one as it has some similarities in terms of the problem even though it's a quite different type of mining: https://www.academia.edu/403594/Application_of_Conditional_Simulation_to_Quantify_Uncertainty_and_to_Classify_a_Diamond_Deflation_Deposit

DeleteTom, thanks for the reference. I downloaded the paper but it's much deeper than my abilities. I did notice toward the end though that Conditional Coefficient of Variation (CCV?) for Measured/Indicated resource is 0.4 or less.

DeleteI believe SRK (Marek Nowak, Vancouver - a geostatistition that I have a lot of time for.) are familiar with CS and use it from time to time.

Bill, I selected this example in particular because it explains everything clearly and does not skip a description of some critical steps based on assumption the reader is familiar with the method. A careful study should reveal the manner in which this could be applicable to Brucejack in helping define more accurate block grades and mining shapes in the resource model itself. I agree that Nowak is a proponent of using similar approaches (e.g. in arguing for the importance of conditional bias). Had he been responsible for this resource there would have been fewer problems.

DeleteMIK seems to be popular in Oz for some reason. A property I studied used MIK on 25/25/10 m main blocks with 6.25/6.25/5 m sub blocks. This had two impacts...it reduced the tonnes of ore (consequently increasing the tonnes of waste) and fluffed up the grade in remaining blocks by about 20%. It looked great on paper but an operator needs to ask how small can one effectively differentiate ore from waste in blasted rock that no longer sits where it was when it was solid, and where the shovel rill angle on the bench is maybe 50 degrees, so the bottom of the bench is in one block and the top of the bench is already in the next one. The property owner felt that a smallest mining unit of 6.25 meters was reasonable, but the shovels he planned to use had buckets that were 6 meters wide. I can imagine the chief engineer and mine superintendent trying to justify to the BOD a reconciliation of 80%.

DeleteYes this is a very common problem where a model has a hazy cutoff boundary and does not take mining shape or SMU properly into account. Happened at Grouse Creek in Idaho for Hecla as well ... I doubt anybody who remembers AND understands what really happened there (and having been over 20 years ago it's a shrinking list) is a shareholder in PVG at this point.

DeleteI think that Brucejack will be a good, cash flow positive gold mine ten years from now. But the current equity holders will either no longer own the mine, or be severely diluted. That is what huge debt load does to even a good project that can't perform to plan.

ReplyDelete