Short High-grade Inconsistent Type intercepts are a bit of a curse for gold exploration. You get a great hit, but when you follow-up it suddenly disappears.

There are many reasons for SHIT intercepts, but sometimes drilling gets cursed by the golden drill-core vein snakes, those little b*stards that wriggle up a drill rod. they are skinny little buggers, but can give you a few meters of great grades and then they bugger-off.

Like this one, I snapped from a gold project I've been working on recently.

mmmm, grey

This little beauty, the rarer North American SHIT vein assayed 10.7 g/t Au over 3.1m (core length).

Here is an annotated version.

Typically, half of the core goes for assaying and half is stored. When they collect a sample, they cut (or as this is the US and they live in the olden days - use a splitter) down the axis of the drill-core (blue line in the photo above). What happens when you have a vein running up the axis of the drill-core is that you will be biasing the assays with high grade mineralization, and leading to an abnormally wide, high grade zone, that is clearly caused by a couple of 1cm wide veinlets.

The nice thing about SHIT intercepts is that for the FAG (the Fraudulent Angry Geologist) they give you an opportunity to pad your PR with some MAXIMUM IMPACT (tm) BS, by letting you:

Report a nice high-grade SHIT intercept - everyone loves those

As a bonus you can call it a new "structure" - have some fun, name it after your girlfriend

Even better - as you only have a single hole, it is "impossible" to calculate a true width, because, you know, GEOLOGY!!!

The other issue is that they can cause chimping (a photographer's term) in the exploration manager (i.e. pointing his finger at the red colored stuff and going "Ooo ooo oo!"), who makes you go back and drill some holes around it (as it could be good), against your advice, that hit nothing, and leads to the inevitable question - "why did you drill those holes".

You often get companies reporting some really high grade assays from underground channel sampling or from drilling, but you need to check the true widths. We often see companies smearing out grade from narrow high-grade veins to bulk up their appearance, but another extreme is going for grade.

In this scenario, you report all the narrow high-grade zones to show that you have lots and lots of great hits so your assay table is full of nice bold and red text (remember - red = good)

Here I'm using the latest results (10 holes) from Orex Silver and the JV drilling at Coneto as an example (link). The drilling intersected multiple veins, including several previously unknown structures.

You can see that they highlight all the assays that are:

>1 g/t Au

>100 g/t Ag

Lets do some excelling

results from 59 samples reported

19 samples >100 g/t AgEq

11 samples >1g/t Au

10 samples >100 g.t Ag

This is what you would expect to get from an initial phase of drilling on a narrow vein deposit

Note: A total of 83 holes has been drilled at Coneto, so this isn't an early stage project.

We also can see that Orex have reported everything as we see some stunning results like:

0.65m @ 0.01 g/t Au and 0 g/t Ag

27m @ 0.02 g/t Au and 2 g/t Ag

3.66m @ 0.03 g/t Au and 2 g/t Ag

Typically in press releases companies report a summary (or sub-set) of the results - for example assays containing >0.25 g/t Au or 100 g/t Ag or something similar. I'm not sure why Orex reported everything, it does show that they have multiple structures, but most are very narrow and low grade.

Why don't we have a closer look at the 'high-grade samples' (the ones grading >100 g/t AgEq)

some monsta hits

Look closely at the true thicknesses. As you would expect, the highest grade samples are typically the narrowest, but at Coneto they are very narrow:

950 g/t AgEq over 10cm

that is the length of a flaccid penis

or for people without penises (or penii) - that is the width of your palm.

The average thickness for a sample containing >100 g/t Ag is 0.59m

If you calculate a AgEq grade over a 1.5m mining width (last column)

only 2 intercepts (highlighted in yellow) are >200 g/t AgEq cut-off grade for an underground operation.

Here it is graphically, you basically want the results to be in the top right corner (wide and high-grade). If they aren't, then it could be time to look elsewhere.

top right = good

So we see here that even though there are a reasonable number of high grade samples, the majority come from very narrow structures, and nothing is indicating the potential for thick-high grade intercepts.

Serbia hasn't been this popular since 1999. We've lusted over the intercepts that Reservoir had been reported prior to their takeover by Nevsun, and so many junior companies are heading there to hope that there are other world-class deposits to be found while enjoying a glass of Italian Riesling.

you want to be in the turquoise and moldy lemon colored areas.

We can see that there are a lot of deposits, and mineralization types, but only a few would you class as being any good.

Bor - 2.1Gt @ 0.64% Cu and 0.24 g/t Au

Majdanpek - 1Gt @ 0.6% Cu and 0.35 g/t Au

Chelopech - 60mt @ 1.2% Cu and 2.4 g/t Au

Timok - 1.7Mt @ 13.5 % Cu, 10.4 g/t Au and 35Mt @ 2.9% Cu, 1.7 g/t Au

The rest are decidedly average, but it is important to note that ALL the best deposits are found in the early morning-urine colored belt in the NE of the map (where the world Bulgaria is located)

This isn't where Tethyan have their projects. Gkcanica and Suva Ruda are found in the orange Vardar Zone that hosts some medium-sized low grade Cu-Au deposits, like:

This doesn't mean that there isn't a large deposit lurking somewhere in this belt, but does indicate that:

It ain't elephant country, mate

Summary

Small low grade porphyry Cu-Au deposit drilled at Rudnitza with

Narrow zone of supergene enrichment

Mineral belt isn't well-endowed

Nothing here screams "major discovery", some average exploration holes, and it will be interesting to see what Tethyan do next. Will they stay-married to the project - keep spending more and more money on it as they have nowhere else to go, or start to do some regional exploration to see if they can find something better?

Geology

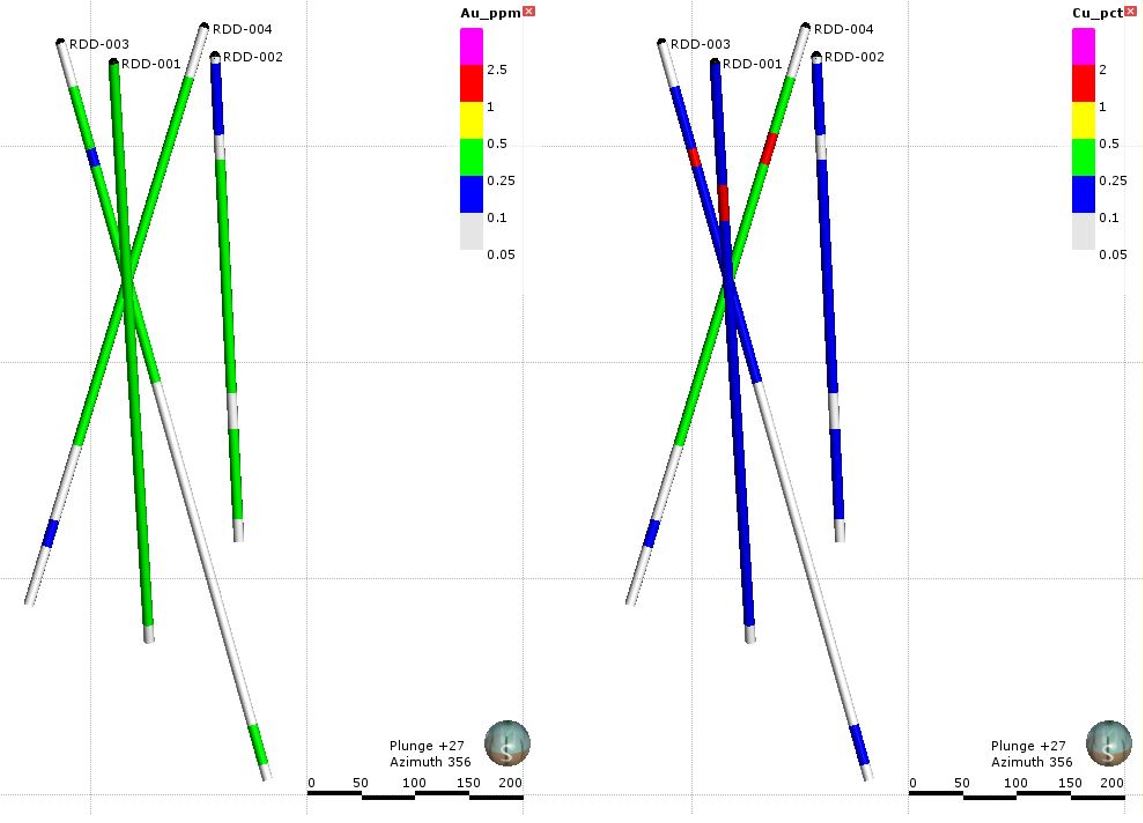

I am interested to see the relationship between the recent drilling and the drilling conducted by Phelps Dodge in 2004, especially holes PDRC-04-03 and 04. I'm going to guess that this drilling was designed to confirm the grades seen in those holes (does this old data exist?) and to see if mineralization continues to depth. Here are the new results:

Reasonable for initial drilling

A cursory glance at the data shows that for an early stage project, this is the first drilling, they hit some interesting grades, particularly gold (some consistent, sub-economic grades on its own) with a narrow zone of high-grade copper zone relatively close to surface.

However, if you take a bit of time and look at the maps and sections on the webpage (link), you can quickly see that 3 of the 4 holes have drilled the same rock from 3 different directions, and a single hole (002) has explored for the continuation of mineralization 100m along strike, where we can see the grades drop-off considerably (3D model here - link)

Left = gold, right = copper

Here is an annotated section, and you can see that all Tethyan have is a small, poorly mineralized porphyry deposit.The small high-grade supergene zone looks interesting, but is small and restricted to the porphyry. The main body is too low grade to really warrant further work, and the 'deeper' zone, is too deep and low grade to really be of interest.

I guess they were trying to 'better understand' the mineralization, but it is frustrating that a company that has spent all that time and money on permits, building access roads and drill-pads that they didn't do something a bit more dynamic. Why drill the same rocks from three different directions?

Let's be reasonable, we are talking about a junior exploration company, funds are tight, they had a well mineralized hole (visually) in hole 001. They did a step out (hole 002) 100m away, and it didn;t get much. So, I assume they panicked, played it safe, and went back to poking around hole 001 to make that they hit something. It keeps the risk low, but also minimizes upside.

Without having some regional geophysics maps or regional geochem it is hard to gauge the potential outside the Rudnitza porphyry. Normally companies drill the best target first. so if that is the case, they may want to spread their wings and see if they can find something better elsewhere.

So, imagine that you have just finished hole 002, it was bad, and you are thinking "what the feck do I do now"? What would a weaselly geologist do?

Here is my alter-ego, FAG (the Fraudulent Angry Geologist), and ask him - what BS can be spun from this project?

We have to assume that the FAG has 1/4 a brain-cell and is evolved from stoats

Remember - if you are investing in Junior Mining stocks, you are the Rabbit!

You saw that there was some good stuff in hole 001, not much in 002, so let us re-imagine the drilling, taking the ~1200m that was drilled in holes 003 and 004 and see what we can do!

We know that the deeper mineralization is low grade, so why not focus on the near surface supergene zone, this can be drilled with a few 150-200m long drill-holes.

proposed holes in red - >0.5% grade shell in yellow

Plan view

That would have allowed you to release lots of press releases with 30-40m @ >1% Cu and >0.3 g/t Au. Imagine those CuEq and AuEq PR headlines, that would suck investors in.

Even better, if all 6 proposed holes hit the high-grade supergene zone you could do a nice BS resource report to define a small (200m x 200m x 30m) resource (3.25Mt @ 1% Cu or 70 million lbs of copper), and start promoting the heap leach potential. the opportunities are endless!

I apologize, I was farting around with Blogger and deleted the original post - so from now on I'm the SAG (Stupid Angry Geologist), please excuse me, I'm off to find someone to blame.....

Here is the original post:

Wellgreen - this is going to be easy, we already know that it is

going to be crap, because...

I also like the way that they go out swinging and compare Wellgreen with a load

of other Ni-PGE projects and mines, and show that it is low grade very

low grade. Prepare to be blown away by the truly awe inspiring grades....

Nickel

PtEq

Feck, don't you hate it when you leave your Ni-PGE project in your

pants pocket, it goes through the wash, and you find that all the metal has

been washed away? BTW - smaller bars are not better, but the presentation does

give us some useful advice - "avoid Northmet".

I like to compare exploration projects against active mines, basically to see

if they are good enough to go into production. We can check Wellgreen against

the results from the Kevitsa Mine (Boliden - Finland):

look at how much money they don't make....

So Wellgreen's

message is - "Buy our shares, our project is worse than a break-even

mine".

I also got a good chuckle on how they calculated the equivalent grades

NiEq - from Ni, Pt, Pd, Cu, Au, Ag, Rh, Co

Maybe they should have included Mn for fun? Everyone one

loves Mn....

They used some high metal prices in the PEA, so at

today's prices (bold), it is definitely uneconomic.

Au = $1250/oz ($1204.1/oz)

Cu = $3/lb ($2.62/lb)

Ni = $8/lb ($4.55/lb)

Pt = $1450/oz ($940.9/oz)

Pd = $800/oz ($754)

Heck, the metal

prices used in the PEA were nowhere close to the current metal prices, a

typical, fudge the numbers to make sure the deposit seems economic and hope

that the readers are too stupid to understand.

It is so lucky that

the project is located half-way to the north pole and require a large CAPEX....

Let us look a bit closer at the resource, maybe there are a couple of higher

grade areas that could be expanded?

NiEq Grade distribution

PtEq Grade distribution

So, there are a couple of teeny weeny higher-grade zones. Nothing out of

this world, and the resources can be expanded to the east (left in the image

above).

At depth they like to show a lot of upside, telling us that lots of holes ended

in "high-grade"

look at the cyan line - the PEA stage 5 opportunity pit outline

It isn't that special, yes, they can expand some of the deeper

mineralization, but that it going to significantly increase the amount of waste

rock (outlined in black) they have to move, and that cost will kill a marginal

grade deposit.

Wellgreen do have a decent amount of cash, but the Wellgreen deposit has been

well explored. There is upside to outline more resources, but what they really

need to do is try and find a high-grade zone, because having "more of the

same" (i.e. lots of low grade crap) isn't going to help.

You need to look beyond the big resource numbers and look at the grade and ask

yourself - Where is the upside? If you are wanting to bet on Nickel, go for it,

but the mineralization at Wellgreen is going to sit in those hills until the

next glaciation.

Conclusion: With the phrase “One Of The Largest Undeveloped (insert metal of

choice) In The World” we have a hack, a short-cut to know when a bunch of

mining parasites are trying to rip us off. So if you see it in company

literature, in a promo pump or perhaps quoted by a CEO in an interview, you now

know what to do!

Otis Gold was forwarded to me by a reader (JLB) and they recently announced that Agnico Eagle has decided to invest ~$5M in Otis (link), so what are AE investing in?

Summary.

Kilgore currently contains a small, low grade resource (2012 - link)

47.5Mt @ 0.53 g/t Au or ~820Koz contained gold

There appears to be some potential issues with drill-hole assay data

Resource calculations appear to be overly optimistic

Recent drilling have returned some decent grades (link and link), but they look to be minor step out drilling from earlier holes, and

Best hits appear to have come from narrow, vertical high grade zones - so probably won't be very large

Kilgore is interesting, there are some issues that need to be resolved ASAP. Personally, I would like them to start drilling the other targets around the property as I can't quite see where they can expand the current resources to where it would be >2Moz Au. It would be interesting to see AEs take on the project....

Background

Kilgore was essentially dormant from 2012 to 2015, when Otis managed to raise some funds and have been drilling the deposit on and off since then. Here is the location of the recent drilling:

We can see that:

The majority are infill holes - i.e. drilled within the limits of known mineralization. This is done to:

This provides more information to better understand the mineralization - change the QUALITY but not QUANTITY of resources (i.e. move inferred resources into the M&I category)

New interpretations may have identified new targets. Infill holes maybe drilled to a greater depth to test these ideas (2 targets tested with 1 hole approach)

The historic drill data is missing/incomplete/low quality and new holes are drilled to confirm the historic data, so that the old holes can be used in resource calculations.

Low risk drilling - get some decent grades for the press releases.

A small proportion are minor step-out (up to 100m) drilling looking to expand the mineralization where it hasn't been fully closed-off.

So, not very adventurous, but when you look through the technical report you see this:

so potentially a third of the assay data at Kilgore is suspect

Visually

you want the sample points to plot close to the green line

This simply says that the RC drill samples, on average returned twice the gold grade than diamond drill samples from the same area.

Here is what they say in the technical report

RC and core assays do not compare well, with paired data comparisons and separate estimates showing that RC assays are higher than core. Issues are identified with both types of data which will not be fully resolved without collecting bulk samples. The various operators of the project have been alert to recovery and sampling issues and appear to have taken measures to reduce sample bias, reflected in the core drilling techniques used.

and this

So I'm guessing that the bulk of the drilling was done to resolve these issues and 'remove' the RC drill-data for future resource calculations. This was a sensible thing to do, but I was surprised that they were able to calculate a Indicated resources with these issues.

Why don't we look a bit more at the 2012 resources

Have any tricks been used to make the resource appear bigger and better? Yes....

Trick 1 - The use of an unrealistically high gold price - In this case $1650/oz.

If you use a high gold price, you are saying:

Your rock is worth more (i.e. more bucks per tonne), and assuming 100% recovery, a tonne of Kilgore 'ore' is worth

@ $1650/oz = $28.12/tonne

@ $1500/oz = $25.56/tonne

@ $1250/oz = $21.30/tonne

You need less gold to cover the mining and processing costs, which means you can use

A lower the break-even/cut-off grade

where $value of gold in rock = extraction costs

You can easily see through this trick by checking the gold price used in the resource calculation against long term metal prices (e.g. Kitco's 5 or 10 year charts), and simply draw a line on it for the assume metal price, like I have done here:

thick black line = $1650

Since 2012, there have been 7 months where gold prices are >$1650, and even when the report was being written the gold price was ~$1600/oz. A more realistic conservative price would have been $1500.

Trick 2 - The use of an unrealistically high recovery - 90%

If you use a very high recovery, again, you increase the value of gold in the rock:

Kilgore - average grade = 0.53 g/t Au

Recovery = 90% (recovery used in the cut-off calculation in the 2012 technical report)

1 tonne of 'ore' contains

0.53/31.1 = 0.017 oz/t Au

0.017 * 0.9 = 0.015 oz/t recoverable gold (the rest is lost)

0.015 * 1650 = $25.3/tonne

@ 80% recovery = $22.50/tonne (11% less)

@ 70% recovery = $19.68/tonne (22% less) and so on

So where did Otis get this 90% recovery value? They must have got it from the various metallurgical studies they have conducted at Kilgore:

2010 study - average recovery = 78.7% recovery

2011 study

Average Recovery = 79.45%

Average grade of metallurgical samples = 1.12 g/t Au (or 211% of the average grade)

2012 study - average recovery = 56%

Note: these are arithmetic means, we can see that recovery varies by rock type, grade and how coarse the samples were, which is normal for all deposits.

You can see that recovery >70% after 30 days of leaching, and never gets above 80%

Same rock, but now oxidized = we can see that a finer grind = higher recovery, but still no 90%!

So, the highest recovery they got from actual studies was ~80%, but in the 2012 resource calculations they've used a very high gold price and an unrealistic recovery value - this means that the cut-off they used is artificially low.

Why is this a problem?

Well, in most deposits, grade follows a simple distribution:

A small amount of high-grade

lots of low grade

In many technical reports they include a simple grade-tonnage chart, where you can see how much of the resource occurs above different cut-off grades. Here it is for Kilgore (note that they use imperial units, and I've added some annotations).

As cut-off grade increases, tonnage decreases

Blue line = amount of material at each cut-off grade

Dark red line = average grade of the resources at each cut-off grade

Green line = total ounces in resources at each cut-off grade.

0.00 oz/t cut-off = 74.1 mt @ 0.009 oz/t Au or ~660koz

0.007 oz/t cut-off = ~30mt @ 0.018 oz/t Au - or 520Koz Au - 60% drop in tonnes and a 22% drop in contained ounces

0.015 oz/t cut-off = 12.2mt @ 0.028 oz/t or 337Koz Au - 84% drop in tonnes and a 49% drop in contained ounces

0.03 oz/t cut-off = 3.5Mt @ 0.045 oz/t or 158Koz Au - 95% drop in tonnes and a 75% drop in contained ounces.

So you can see there is lots of low grade, but significantly less high grade, and you can see why companies want to use as low a cut-off value as possible - as it means that they can include lots of the low grade material into the resources, but this has 2 effects:

Increases the tonnage and contained ounces, but

decreases the average grade of the deposit

So you end up with a big, crap deposit.

However, you can do a bit of maths and using current metal prices ($1250/ounce), and real recoveries (80%), we can try and calculate a new cut-off grade, so see what could happen to the resources.

I've assumed that mining and processing costs will be ~$10.5/tonne (from the technical report), and from this we get an updated cut-off of 0.01 oz/t, which from the grade-tonnage chart means we have (M&I):

20.6mt @ 0.021 oz/t for 441Koz contained gold, or in real units

18.7Mt @ 0.72 g/t Au

So we have gone from 520Koz Au down to 441Koz, so goodbye 80Koz Au, it was nice knowing you....

So, It will be interesting so see what values Otis use in the updated 43-101 slated to be released this year?

Geology Wank

We'll ignore this for now and have a look at the assay data. I've only been able to work with the recent drilling data, and you can download my model from here (link)

Here is a generalized section through the deposit, look how the gold resource is centered on a fault, and extends into the lime green Tlt (Lithic tuff), so we should see 2 control on mineralization:

A vertical, structural/fault control on the high grade (>1 g/t) mineralization

A horizontal, control on the low grade (<1 g/t) mineralization - this is probably due to lithology (contacts between rocks), a sill etc.

I was quite surprised to see this in the 2012 technical report:

It appears that to calculate the resources, they have used a simple, global trend (black line), and when you look more closely, you can see that the high grade zones (red) that don't quite fit together, and occur as random splodges. This suggest that the high-grade mineralization is probably controlled by vertical structures and using the general trend, may have overestimated their size in the 2012 resource.

This is what they say in the technical report

Kilgore drill orientations are locally limited due to permit restrictions and topography. The drill hole orientation is not optimum for the capture of structurally controlled mineralization. Some drill holes are oriented along mineralized structures, whereas others miss it altogether because they are drilled parallel to them.

This means you can have a really nice, long, high-grade intercept that came from a hole drilled down the middle of a structure, and in an adjacent hole, get nothing. If that is the case, you have to be really careful about modelling the grade, you CANNOT use a generic trend. but let us look at the data in 3D, I only have the recent drilling data (i.e. drilling since 2012), but it is useful:

A long section

Left - to the SE, right - to the NW

We can see an fault offsetting mineralization. This means that to the left, mineralization appears to be open, but getting deep (>150m depth), and to the right (NW) the mineralization appears to have been eroded away.

Here are some cross sections, and look how the grades change between drill-holes.

You can see that the highest grades are very restrictive, and I feel they relate to vertical faults and structures, and the gold is bleeding out along the rock contacts to form a low grade zone around these high grade structures. and this is what happens to the grade shells with different generic trends.

No trend - Leapfrog looks in all directions equally

Horizontal (Lithology) trend - Leapfrog biases the search along the black line

We can see that the high-grade some is a bit bigger than before.

Vertical trend - bias along vertical structures

High-grade zone a lot smaller

So you can see, very quickly how changing the trend on how the grade shells are created can have a drastic impact on the amount of resources calculated, and you have to be very careful and make sure you understand the controls on mineralization. In many cases you can't use a generic trend.

So we have a small, low grade deposit, with issues, and overly optimistic historic resource.

Upside Potential

Otis and previous companies have conducted a lot of exploration at Kilgore that have identified several other targets.

There has been a lot of drilling outside of the Kilgore deposit.

And form the map above, they have identified erratic gold mineralization, up to 52m @ 1.25 g/t Au. I don't know if these holes have been followed up, and as they are RC holes, the grades are probably suspect, but it does show that there is gold and there are some good starting points for drilling in 2017.

Do I think that they can define >2Moz at Kilgore? I think that is an upper limit, and the 2017 updated resource calculation will tell me how wrong I am.