For the discerning investor it is hard to push beyond the huff and puff in the PRs as every gold project seems to be brilliant. they all have very low costs (cash, AISC), great returns (IRR and NPV), Ana Paula looks to be different, Timmins tell us, AP is:

- Cheap to Build - $121.7M

- Great Grades - 2.24 g/t Au over the life of the mine

- Short payback period

I worked through the figures to see if I could understand a bit better why the figures for AP are so good, after seeing some nice 'tricks' in the Corvus PEA, I wanted to see if anything untoward was happening with AP.

The short answer - No, but the economic model is probably a little over optimistic. AP is a good project, and IF Timmins don't mess it up, they could have a nice long line of suitors looking to acquire them (e.g. Torex, McEwan, maybe even Tahoe?).

The short answer - No, but the economic model is probably a little over optimistic. AP is a good project, and IF Timmins don't mess it up, they could have a nice long line of suitors looking to acquire them (e.g. Torex, McEwan, maybe even Tahoe?).

I found some minor issues with the economic model:

- Milling rates - they assume that they will be operating at full capacity for the entire year

- No commissioning period - they are operating at 100% from year one.

- 5% discount rate is fashionable, but 7-8% would be more realistic

- $0 working capital

One question you have to think about is how will Timmins fund the development of AP?

It looks like they can do it just from the revenue from San Francisco, which is generating ~$12M/quarter (at current metal prices), and they have ~$82M in equity (only ~$12 as cash), so if they are careful and don;t have any issues at SF, then they won't need to raise money by either diluting the crap out of their shareholders or borrowing money at crippling interest rates.

Let's run through the AP Economic model.

Capex

Timmins have worked hard on reducing the Capex for AP by:

- Buying the El Sauzal mill from Goldcorp for $8M (cash and shares)

- Using contract miners so they don't need to spend capital on buying a mining equipment

- this will lead to slightly higher operating costs

I went through and checked the numbers, and compared them against a couple of other operations and CAPEX values for open pit gold mines in Mexico, and they are inline with other operations.

- Penoles built Velardena, a 6000 tpd underground mine for US$203M

- Torex built El Limon, 8000 tpd for $790M

- In comparison - Ixtaca (Almaden) CAPEX of $100M for a 8000 tpd operation looks to be unrealistic.

Working Capital

The only minor issue I found was the way working capital is handled. They have a small amount ($6.9M in year -1), but that is all returned in year 9 (when the mine closes), so it balances out. However it should mean that AP capex should be $6.9M higher at $128.6M.

I also feel that the working capital should cover 2-3 months operating expenses, around $15M especially to cover that tricky start-up period.

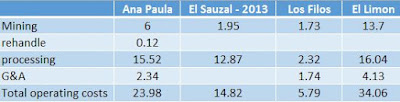

Mining Costs

Lets check the costs that Timmins are using - how do they compare to operating mines?

And visually

|

| Ana Paula - PEA values, other = actual values from MD&As |

They look OK, there are some differences because:

- El Limon has a higher mining cost due to its higher strip ratio

- Los Filos is an open pit mine and they recover the gold via heap leach (no milling)

- El Sauzal costs are from 2013 and don't have values for G&A.

Nothing major, these costs are good and inline with current (and recently operating) mines.

Possible Issues

I've worked in some possible issues into an updated Economic Model to see how they could impact the NPV and IRR for AP.

1. Mill throughput

They bought a second-hand mill from El Sauzal, I know that it will be nicely rehabilitated and probably painted a beautiful shade of yellow and blue (or red or utilitarian grey), and they are expecting to:

- process 2,160,000 tonnes/year at 6000 tpd plant

- 2,160,000/6000 = 360 days/per the plant is operating at full capacity

- or the pant will be operating at 5918 tonnes per day, every day.

So they are expecting to use the plant at full capacity for 360 days a year (I'm assuming it will get days off for Christmas, New Year, Easter, Independence day, and either Revolution Day or Benitio Juarez's birthday. That sounds a bit to perfect, was the plant that good when it was at El Sauzal?

|

| not quite, but close |

It wasn't bad, it average 350 days of operation per year at peak capacity, so if they maintina the same standard at AP, you would expect them to 2.1 Mt/year.

2. Commissioning

Mines and mills take time to start operating at peak capacity. At El Limon, they still haven't quite reached full capacity (they are up to 83% of design - link), so will you get a similar 6 month commissioning period at AP?

3. Discount rate.

5% is cute, I like to check the discount value against the interest rates that various loan/financing are being arranged at.

- Premier Gold - loan from Orion mine finance at 6%

- Lydian - Libor + 6.5%

- Red Eagle - Libor + 7.5%

So if you are borrowing money at libor (currently at 1.5% for USD) + 6.5%, then a 5% discount rate seems low, a rate of 7-8% looks a bit more realistic.

4. Working Capital

In a nice stroke of excel, AP has no working capital in its advertised CAPEX.

|

| who needs working capital? |

So how are they going to pay for the operating expenses for that tricky start-up period while they are waiting to receive revenue from their first shipment of dore? A study done of gold Australian mines shows that it took on average 47 days to receive payment (link), maybe in Mexico it will be quicker, but it would be nice to see Timmins include ~$10-15M to cover this.

My mistake, they do, they have $6.9M in year -1, but like the deposit you give to the bottle shop/off-license/liquor store, when you buy a beer (or IRN BRU) in a glass bottle. When you return the bottle (or in this case - close the mine), you get that money back, errr, 9 years later.

So, the real CAPEX is actually $128.6M.

All this data when into an updated Economic Model with the following assumptions:

This isn't my area of strength, but it still shows that Ana Paula is a good project, just not quite a spectacular as advertised, but robust enough to pass the stress test and I do like the fact that Timmins have been conservative with the metal recoveries.

I think this is a good project for Timmins

- Mill operating at 6000 tpd for 350 day/year or annual throughput if 2,100,000 tonnes

- 7.5% discount rate

- 6 month commission period (using El Limon as a guide)

- mill operating at 75% capacity, increasing to 100% afterwards

- Working capital of $15M (to cover 3 months operating expenses)

The results are:

- CAPEX increases to $136.7M

- Pre-tax

- NPV decreases to $296.6M

- IRR decreases to 45.13%

- After Tax

- NPV decreases to $180.3M

- IRR decreases to 21.98%

This isn't my area of strength, but it still shows that Ana Paula is a good project, just not quite a spectacular as advertised, but robust enough to pass the stress test and I do like the fact that Timmins have been conservative with the metal recoveries.

I think this is a good project for Timmins

First one to say : Thank you. I bought more few weeks ago during the dip since i felt AP was a good one. Your take on AP helps me now to increase my position size since I feel more confident about the project. SF mine will be operating during the first year of AP so working capital should not be an issue. I imagine, TGD will have around 15 million at end of 3rd qrt.2016

ReplyDeleteAt present, thank you. but in future beer on me.

Thanks for your report. Sorry, at what price gold was your assumptions based? I'd give it a better than 50% chance this project will be taken-out after the FS comes out. If not taken-out, as stated in the corporate presentation, management believes the AP project to likely be a highly financeable project, and with SF generating ~ $12M/quarter (at current metal prices), Timmins treasury should not only be sufficient to cover start-up working capital, but also help to reduce the final amount needed in financing the CAPEX. Thanks again for your report.

ReplyDeleteHello Blue,

DeleteThey were based on $1200/oz Au and $14/oz Silver - which are the figures used in the economic model in the 2016 PEA. Obviously, at higher prices the NPV and IRR increase significantly.

I like the fact that Timmins have worked to reduce their debts (currently at ~$1M), and if they can keep SF churning out cash they will have enough to cover the construction costs at AP.

They have $82M in cash and at current metal prices they are making $12M at SF.

by the end of 2016 their cash balance should be: 82+12+12 = $106M

by the end of 2017 it should be around $154M - which covers the CAPEX, working capital and leaves ~$20-30M spare.

Hopefully, they won't need to do a financing (their debt or issuing shares), but i posed the question so that people think about how a company will raise money

1. debt - potentially at a high interest rate, and if you look at some of the deals that Orion has done, streaming deals etc.

2. issuing shares - leading to dilution.

The big question will be, when will someone take over Timmins? Once AP is up and running? or just a bit before?

Great post as always TAG. I wonder, if someone did make a move for Timmins, who would it be? I think its a bit too small for the majors or even the 500K+ intermediates, so a producer currently producing 200-300k a year might see this as an interesting asset to add to their portfolio. Who do you think might make a move?

DeleteCheers!

This comment has been removed by the author.

ReplyDeleteThanks for your excellent and straightforward analysis. Arturo has weathered a tough couple of years but has designed and is executing a new lease on life for SF and long term for Timmins with AP.

ReplyDeletePS I think it's a type "Mill operating at 6000 tpd for 350 tonnes/year" i think you intended 350 days / year.

ReplyDeleteIs it true that some parts of Ana Paula have not been drilled yet - so it may have significant inferred resources ?

ReplyDeleteSince you used 1200 usd gold price - your calculations are done here considering the fact that San Francisco was extended to 2023 or not ?

http://www.kitco.com/news/2016-08-23/Timmins-Gold-Extends-Projected-Operations-At-San-Francisco-Mine-Into-2023.html

A.G.,

ReplyDeleteYou mention for Timmins that "they have ~$82M in the bank".

Where are you getting this figure? In both their financials AND their corporate presentation, the number is ~$12-13M.

Am I missing something?

Thanks!

I was looking at the equity figure in the Q2 MD&A, I'll change the post to reflect this

Delete