This is just a quick post on the Camino Rojo sale by Goldcorp, who have taken a large write-down, but where there any red flags that undermined the value of Canplat's asset?

Summary

- Proximity to the property boundary prevented development - drilling by Fresnillo has identified the continuation of the Represa zone and potentially up to 25% of the resources are owned by them

- Metallurgy - generally poor silver recovery

- Oxide ore = ~85% Au recovery but only ~30% Ag recovery

- Transitional = 30-60% Au recovery; 30-40% Ag recovery

- Sulfide - not reported, I'm guessing that Goldcorp has worked on this.

- Mining - 2009 pit only focused on Oxide/transition ore

- Drilling by Fresnillo appears to have found another body, suggesting that additional mineralization could be found in the area

Any development of the main (Represa) zone will need to involve Fresnillo. Can Orla do this, or will their focus be on exploring the property for additional mineralization?

Maybe one option could be something similar to Juanacipio. Do a deal where Fresnillo are the operators and Orla can maintain a minor interest?

Geology Crap

Camino Rojo is an interesting project, according to the last 43-101 filed by Canplats in 2009 it contained the following resources:

|

| A decent resource |

Looking at Goldcorp's Dec 2015 resources (

link), the resources have increased significantly to:

That is a decent increase, they've added ~6Moz Au and kept a similar grade, which is good. However, when we look at where the drilling is located, we can see a major issue:

|

| red line = property boundary |

We can see that the deposit runs right to the edge of the property, and we can see an area of drilling in Google Earth on the other side that indicates that Fresnillo have found the continuation!

We can also see to the NE a second area of drilling that suggests that there are other mineralized bodies in the area. So, if there is a deal to be done, Fresnillo won't be selling cheaply as they could be sitting on >5Moz Au!

I imported the Canplats data into Leapfrog (viewer file

here), to have a closer look.

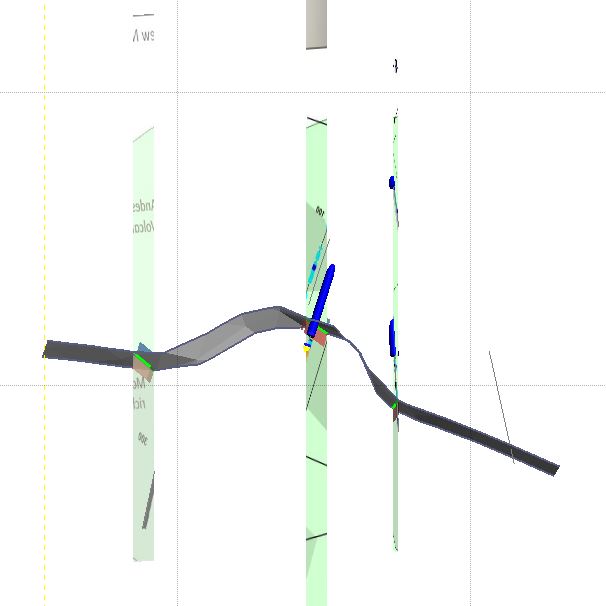

|

| Even the proposed pit crosses the property boundary |

Some sections

|

| Black line = proposed pit; blue line = property boundary |

|

| Black line = proposed pit; blue line = property boundary |

A 3D view

|

| left = Fresnillo; right = Goldcorp |

So drilling defined an Au-Ag zone that is ~650m thick right next to the property boundary, and then, Goldcorp have spend >$100m expanding those resources.

Why were Goldcorp not able to do a deal with Fresnillo to acquire the adjacent concession? Did they want to much? If that is the case, what chance to Orla have on developing the project?

I still think it is an interesting deal for Orla, but when is the game plan? I see 2 options

- Look for more deposits - drilling has found at least 2 and this is a new (discovered in 2008) camp where drilling has already defined >10Moz Au (I'm assuming that Fresnillo has found something)

- Do a JV with Fresnillo with Fresnillo being the operators and Orla having a 40% interest.

We can see that there are a lot of targets around the property, and a well funded exploration campaign could turn up 2-3 new deposits in an emerging camp.